Nobody who owns a Corvette treats it like an appliance. These are cars people research for years before buying, maintain obsessively and park at the far end of lots to avoid door dings. So when one gets hit by a distracted driver or sideswiped on the highway, the damage runs a lot deeper than the sheet metal. Most owners find out quickly that the repair estimate is just the opening number in a much longer and more expensive conversation, one that insurers are generally better prepared for than the people they’re negotiating with.

When a Crash Involves More Than Just Sheet Metal

Pull up the repair history on any modern Corvette claim and a few things become obvious fast. The parts are expensive, the labor is specialized and the shops qualified to do the work correctly are spread thin across most of the country.

This goes back to how the cars are built. Fiberglass has been part of Corvette construction since 1953, and carbon fiber showed up in more recent generations, especially on higher-trim variants. The C8 complicated things further by moving the engine behind the cabin. That mid-engine architecture is a structural departure from anything a conventional body shop deals with day to day, and damage to those components requires technicians who actually understand what they’re working on.

Why Corvette Repairs Aren’t Like Ordinary Auto Body Work

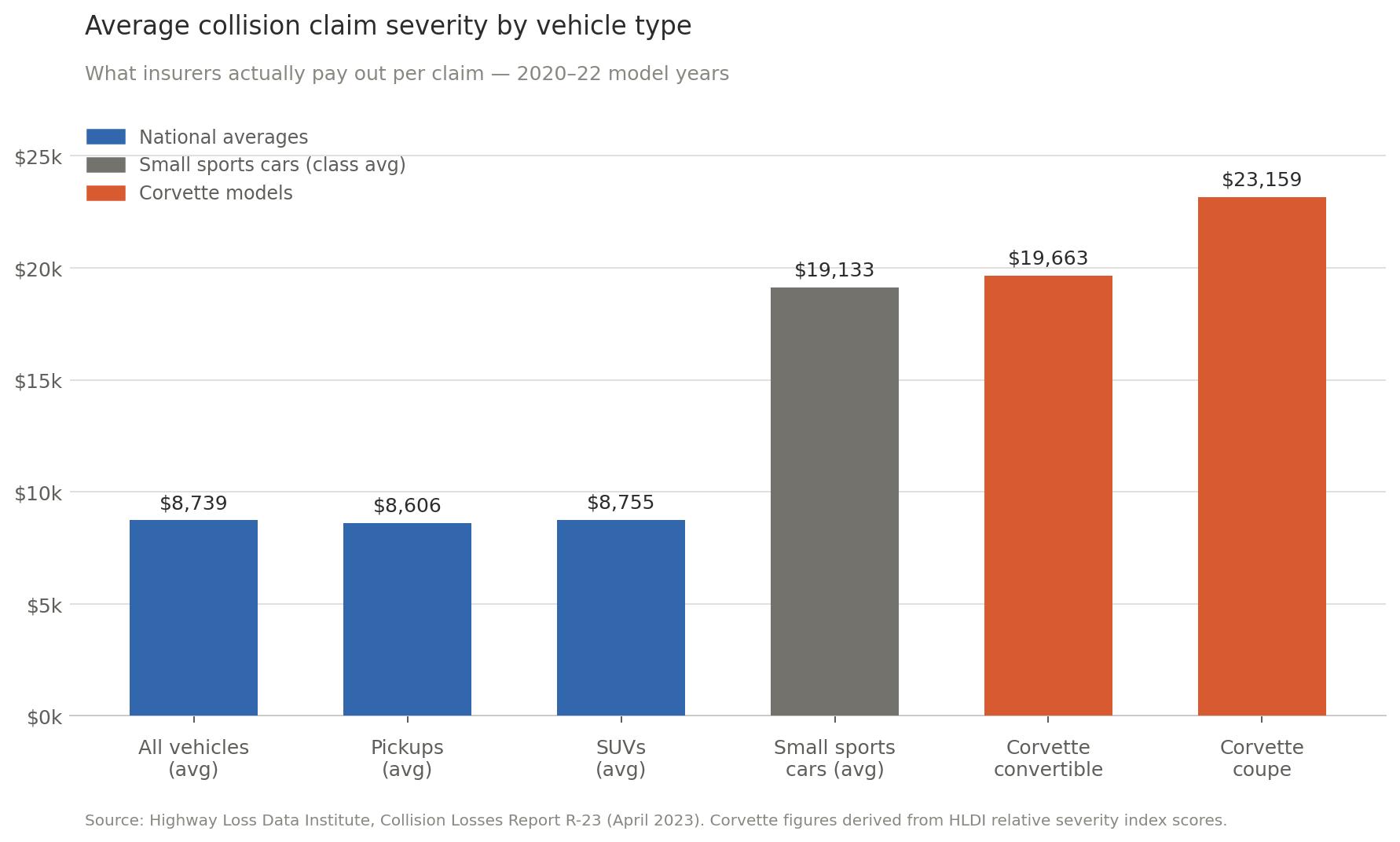

Finding a certified facility isn’t always simple. In a lot of markets, qualified shops are rare enough that owners wait weeks just for an appointment. Parts availability adds to that timeline, and OEM components for performance vehicles aren’t cheap. Research from the Highway Loss Data Institute shows that collision claim severity, meaning the actual payout per claim, runs consistently higher for sports cars than almost any other vehicle category.

That gap gets wider when insurers start pushing aftermarket substitutes. A replacement panel that came from a generic supplier isn’t the same part, and on a car with tight tolerances and a specific finish, the difference shows up eventually whether the owner notices it at pickup or not.

The Financial Hit That Goes Beyond the Repair Bill

The repair estimate gets most of the attention, but Corvette owners who’ve been through a serious accident often say it was everything else that caught them off guard.

Rental reimbursement under a standard policy is built around economy cars. There’s nothing in a typical rental fleet that comes close to what you’re driving, so the owner either pays the difference out of pocket or goes without for however long the repair takes.

If the car has to sit somewhere while a liability dispute gets sorted out, storage fees start stacking up. Injuries bring their own timeline of costs that don’t wait for insurance settlements to resolve. None of this is unusual or unpredictable; it’s just rarely part of the first conversation after a crash.

Knowing the full picture of what’s recoverable makes a real difference in what you actually collect. Car Accident Lawyers in Tampa, FL work with accident victims to identify every category of damages on the table, including the ones the other driver’s insurer has no particular reason to bring up.

Diminished Value: The Loss Most Corvette Owners Never Recover

Here’s something most people don’t learn until after they’ve already settled: a perfectly repaired Corvette with an accident on its Carfax is worth less than an identical car that’s never been hit. That gap is called diminished value, and it’s recoverable, but almost nobody goes after it.

The math isn’t complicated. When a buyer is comparing two otherwise similar examples and one has a collision history, they pay less for it or walk away entirely. Corvette buyers in particular pay close attention to documentation. A clean history on a numbers-matching example carries real monetary weight, and losing it has a cost that exists completely separately from the repair bill. Insurers know this and don’t volunteer to compensate for it.

Pursuing a diminished value claim requires documentation, usually an independent appraisal and some persistence. Owners who don’t know to ask rarely see a dime of it.

What the At-Fault Driver’s Insurance Won’t Tell You

The adjuster handling the other driver’s claim isn’t your advocate. Their job is to close the file for as little money as possible, and they’re experienced at it in ways most accident victims simply aren’t.

The parts argument comes up constantly. Insurers will often spec aftermarket components on a repair and frame it as equivalent to OEM. On a standard sedan, that’s debatable. On a Corvette, where fitment and material quality are part of what makes the car what it is, it’s not a reasonable substitution, even if the insurer presents it as routine. Owners who sign off on the estimate without checking what’s actually being installed may not realize what they agreed to until something doesn’t sit right on the car.

Total loss valuations are another place where Corvette owners get shorted. When repair costs push toward or past a threshold percentage of the car’s stated value, the insurer may move to total it out. The number they assign to the vehicle in that process typically comes from broad market comparables that don’t account for condition, documented history or specific options.

A well-maintained C7 Corvette with a full service record and low miles is a different asset than a generic comp pulled from a database, but the formula won’t necessarily reflect that unless someone pushes back.

Protecting Your Investment Before and After an Accident

The owners who come out of accident claims in the best position usually did some work before anything ever happened. Agreed value policies are worth understanding. Unlike standard coverage, which leaves the final payout to an adjuster’s determination, an agreed value policy locks in a number upfront.

For a car whose value the market may not price accurately, that matters. Thorough documentation helps too: current photographs, receipts for modifications, a clean and complete service record. These things establish a factual baseline that’s a lot harder to argue against than an owner’s word alone.

After a crash, the most important thing is not closing out the claim before the full scope of the damage is understood. That includes the repair, the diminished value and any injury costs still in progress. An independent estimate from a certified shop gives you a real number to compare against what the insurer is offering.

And if the process starts feeling adversarial, which it frequently does when there’s real money involved, having a lawyer involved changes what the other side is willing to put on the table. The insurance system wasn’t built to automatically make a Corvette owner whole after an accident. Getting there takes knowing what you’re owed and being willing to ask for it.